Mortgage / Secured Loan Arrears

- Contact your lender

- Pre-court action

- FCA rules / Pre action protocol

- Court hearing papers

- Preparing for and drafting proposals for the court hearing

- What kind of orders can the judge make?

- Warrant for eviction

- Eviction

- Getting re-housed

- Free independent advice

- Be Prepared Before Getting Advice

For a number of reasons including job loss, relationship breakdown, interest rate rises, paying other less important debts first, many people have got behind with their mortgage and secured loan payments or are struggling in one way or another to maintain them.

Maintaining payments towards your mortgage & secured loans will normally be a top priority expense as failure to do so will usually mean that your home will eventually be put at risk.

If you fall behind with your mortgage / secured loan payments and ignore the situation or cannot come to a suitable arrangement with your lender(s) then they may eventually commence possession proceedings to evict you from your home

Contact your lender

If you have problems paying your mortgage / secured loans, you should contact your lender(s) as soon as possible and try to reach an agreement / arrangement as this may stop them from taking legal action (see examples below)

- offer normal mortgage payments plus an amount to clear any arrears within a reasonable time

- offer sum to clear or reduce arrears plus a payment arrangement as above if applicable

- request a temporary payment break

- discuss the possibility of temporary interest only payments (you only pay the interest on the mortgage loan not the capital resulting in lower payments, this may be affordable)

- discuss extending the terms of your mortgage / possible re-mortgage

- adding the arrears on to your mortgage

- request time to sell the property

- hand back the keys

You may wish to look at ways of increasing your income and check any benefit entitlement as a way of helping with your finances / mortgage payments etc

Time order on a secured loan

A time order could be particularly useful if you have a secured loan and your creditor is threatening to repossess your home.

It can change:

- the amount you have to pay each month; and

- how long the agreement will last.

- In some cases, the court can also make an order to change the interest rate.

Not all secured loans can be covered by a time order (see below).

Pre-court action

Before lenders take court / possession action for arrears they usually send out letters outlining the level of arrears / missed payments etc and requests that you contact them to make up the arrears. If you do not address the situation it is likely that you will receive a formal solicitors letter informing you that an application to court for possession will be / has been made. Lenders will not usually start possession proceedings until accounts are at least approx 3 months in arrears.

FCA rules / Pre action protocol

Your mortgage lender should not start court / legal action against you without following certain rules as set out by Financial Conduct Authority (FCA). The rules say that your lender must treat you fairly and give you reasonable chance to make arrangements to pay off your arrears, if you are able to. They must consider any reasonable request from you to change when or how you pay. Your lender should only start court action as a last resort.

As well as the FCA rules, your mortgage lender should follow certain other procedures before they start court / legal action. These are called a pre-action protocol.

If you are not treated fairly you may be able to complain to the Financial Ombudsman

Court hearing papers

If you do not contact or cannot reach an agreement with your lender(s) and they have followed the correct procedures as briefly described above then they may take you to court for possession / eviction.

If any lender(s) start possession proceedings then you will be sent a claim form by the court informing you of the time and date of a hearing and will also include a form called particulars of claim, this will set out your lenders case for gaining possession of your home. You should also receive a N11M defence form which should normally be filled in and returned within 14 days, however the court should still accept your defence at any time before, or even as late as the day of the actual hearing (please note if the N11M defence form is returned after the 14 day period, the court may order you to pay any costs caused by the delay).

(Always check whether the information is accurate on the court forms you receive.)

Possession Claim Online (PCOL) is HM Courts & Tribunals Service's Internet based service for claimants and defendants.

Preparing for the court hearing

If you cannot come to an arrangement then on the day of the court hearing the District Judge will ultimately make a decision.

If you wish to stay in your home then you will need to defend the hearing and put forward sensible and sustainable offers / proposals to the court for the District Judge to consider (examples below)

- offer normal mortgage payments plus an amount to clear any arrears in a reasonable time

- if applicable, ask for time for DWP mortgage interest payments / issues to be concluded and incorporate a payment offer if necessary

- offer sum to clear or reduce arrears plus a payment arrangement

- ask for time to sell the property

- What is a reasonable time to repay the arrears?

-

Lenders will sometimes ask you to pay off arrears over 12 to 60 months. If this period of time is not affordable you may be able to ask for longer to pay (see below).

If your home is worth more than your total mortgage, tell your lender. An important court of appeal case, Cheltenham & Gloucester v Norgan says that in this situation, a reasonable time to pay back the arrears could be the whole lifetime of the mortgage.

Under this rule when the court and your mortgage lender look at how long you should be given to pay off the arrears they have to take account of how long is left to go on your mortgage.

So, for example, if there are 10 years left remaining on your mortgage term you could be given 10 years to clear your arrears by making monthly payments on top of your normal monthly installment.

At the court hearing the District Judge will ultimately make the decision on the period of time to repay the arrears

You may need to draft a Financial Statement to take to court to show the District Judge that your offers are sensible and sustainable or get independent advice and assistance with this and court representation if necessary.

It can also be very useful to take to court any other evidence to back up your case such as DWP mortgage costs / application & other benefit claims, proof of wages, benefits, tax credits, other income, recent mortgage payments, lender correspondence, evidence of health problems etc, proof that you have had advice.

It is important that you should attend any court hearing allowing yourself ample time to arrive at the court.

You and / or your representative will normally have the chance to consult / negotiate with your lenders solicitor / agent and may be able to come to an agreement with your lender before the actual hearing takes place.

Attending the court hearing will give you the chance to state your side of the story and could give you a better chance of staying in your home.

If you do not already have a solicitor or an agency adviser to represent you, there may be help available at the court via the duty solicitor / adviser desk scheme. You should contact your local court before any hearing date to establish if they operate a duty scheme if appropriate.

The hearing will be held at court before a District Judge who will consider the information and evidence provided by both sides (the lender (claimant) / representative and by you (defendant) / representative) before making a decision.

Other potential defences

Irredeemably unenforceable secured loan agreement.

If possession proceedings are in relation to a pre 6th April 2007 secured loan regulated by the consumer credit act, you may have a defence on the ground that it is irredeemably unenforceable.

Undue Influence

You were given bad advice when you took out the loan or mortgage. This is called "undue influence and misrepresentation".

You should always seek independent advice from a housing specialist, solicitor or other independent agency if you think any of the above could apply to you.

What kind of orders can the judge make?

- decide not to make an order for possession

- makes an order for possession (example 28 days)

- make a suspended possession order on terms

- adjourn the hearing

- make a possession order for some future date to allow you time to move out and find somewhere else to live

- make an order that you give up possession in a very short time

- make a money judgment

If you fail to reach an agreement with your lender and do not attend court then it is very likely the District Judge will make an order for possession in your absence. If the District Judge does make a possession order (for example 28 days) then this does not mean you have to leave the property after the 28 days have expired as your lender will still have to apply for a warrant of eviction.

If the District Judge makes a suspended possession order on terms (example full mortgage plus a monthly amount to clear the arrears) you must maintain payments as ordered by the court, as failure to do so will very likely result in your lender asking the court to issue a warrant for eviction which can be done without another hearing.

If you experience problems maintaining payments on a suspended possession order, do not ignore the situation and let arrears build up, speak to your lender and get immediate advice.

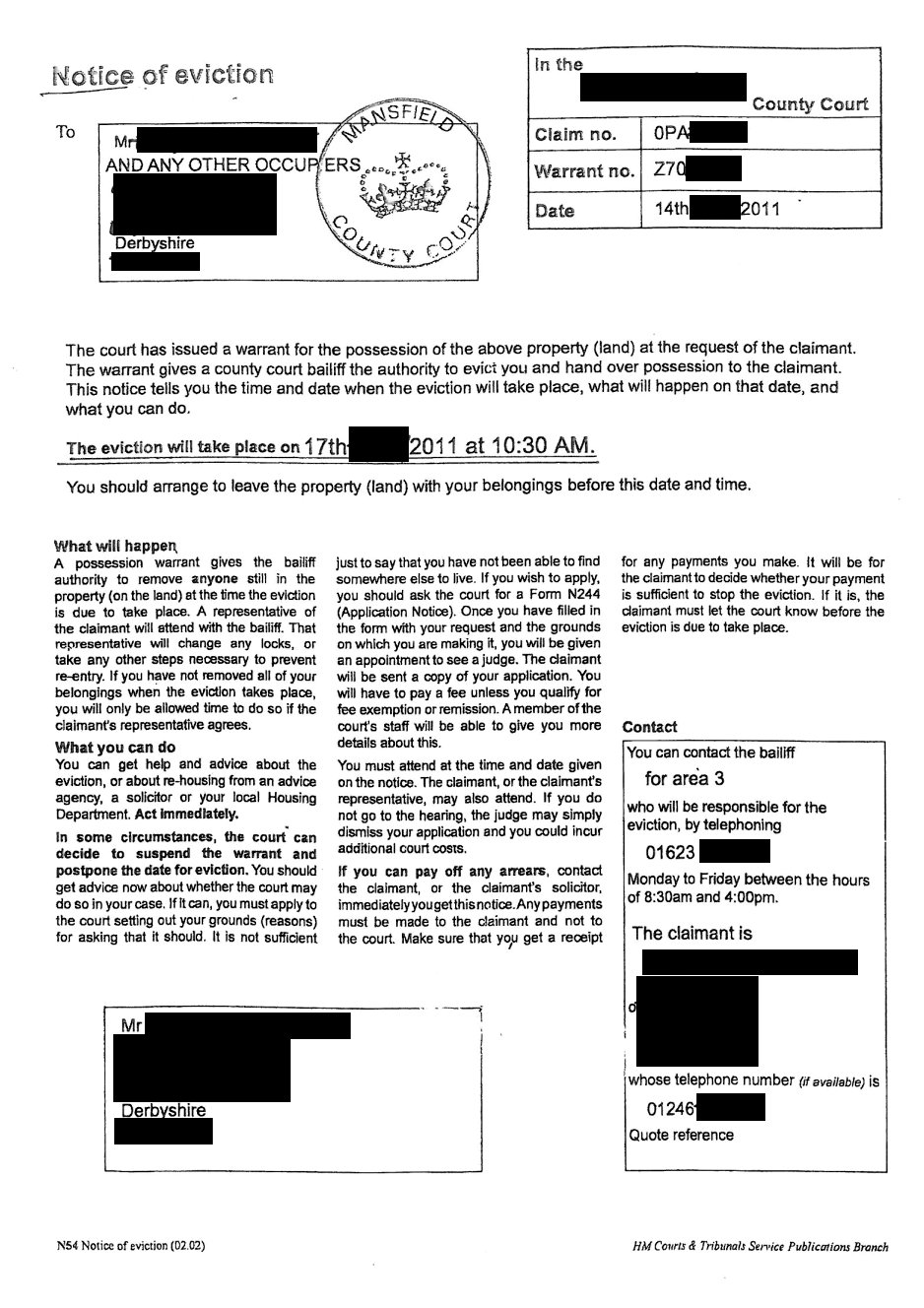

Warrant for eviction

If your lender obtains a warrant of eviction you will get a copy / letter from the court bailiffs informing you of the time and date that the eviction will take place (usually approx 10 to 14 days after warrant issue)

If you receive a warrant as above (or for any reason) you may still be able to stop / suspend the eviction by submitting form N244 to the relevant court (fee payable unless exempt via form ex160) requesting an adjournment or suspension on evidence / proposals / reasons. On receipt of the N244 form the court will grant a hearing (before the actual eviction time)

A the court hearing the District Judge will consider the evidence / proposals and make a decision as to whether adjourn the hearing / suspend possession or order the eviction to take place. If the eviction is ordered to take place you could try asking the court for more time to allow you to get re-housed.

Eviction

If all your efforts to remain / stay in your home fail, you will be given an eviction time and date as already explained. This is really the end of the road and unfortunately on the named day the bailiffs will attend and evict you, forcing their way into your home if necessary (with a police presence if needed).

Getting re-housed

If you are faced with eviction and no hope of stopping or suspending a warrant you will need to look for alternative accommodation as soon as possible. Many people believe that their Local Authority (council) will re-house them when facing eviction. This is not true in all cases due to the intentionally homeless rule or if you are not classed as a priority need.

If you are facing the possibility of possession / eviction or homelessness for any reason contact your Local Authority (council) as soon as possible and ask what they can do for you with regard to re-housing.

You have rights with regard to a homeless interview and there is a homeless code of guidelines your Local Authority (council) should follow with regards to re-housing and the intentionally homeless rules etc. Make sure you know your rights and if in doubt or you are not happy about any decisions etc seek independent advice as you may be able to challenge them.

Free independent advice

If your home is at risk and you have any doubts or not sure about anything seek immediate independent specialist advice from a free recognised agency / solicitor (examples below)

- Citizens Advice

- National Homeless Advice Service (NHAS)

- Shelter

- StepChange (CCCS)

- National Debtline

- Legal Aid

Be Prepared Before Getting Advice

It will greatly assist advisers and could save valuable time if you gather together as much information as possible before any interview.

- What details should I bring with me for advice with mortgage arrears?

-

- Details of all mortgages and secured loans on the property (agreement documents)

- Letters from your lender concerning your arrears

- Type of mortgage / secured loan

- Level of arrears

- Have you contacted your lender(s) about options?

- Details of any Charging Orders secured on the property & payment arrangements

- How much is the house approx worth?

- Was the house purchased under the Local Authority right to buy scheme?

- What the position is regarding equity in the property negative / positive / how much?

- What are the normal contractual monthly payments on the mortgages / secured loans?

- What are the terms of the mortgage payments (example interest only)?

- Are the terms of the mortgage payments set to change (example end of a fixed term interest rate)?

- What is the remaining term of the mortgage (how many years & months left to pay)?

- Can a third party help you with the mortgage / secured loan payments (example family or friends)?

- Have you made a claim for help with mortgage interest payments via the DWP?

- Proof of any recent payments towards your mortgages / secured loans

- Has anyone else got an interest in the property (beneficial / financial)?

- Do you want to stay in the property?

- Is the house up for sale?

- Have you any other debts?

- Details of all your income & expenditure (example salary, pensions, benefits, pension & tax credits, other)

- Have you any savings / assets?

- Have you contacted your local authority housing department regarding homelessness & re-housing issues?

- Evidence of any relevant health issues / problems

What does this mean?

What does this mean? {kind=link}